November 2021 changed Emily Swift’s life. Just a few months before she had started her own

film lab, the struggle to stand out, and living on a steady diet of ramen noodles, was getting to her. Then Swift heard about non-fungible tokens (NFTs).

“I couldn't watch my friends make all this money and not get in on this,” she says.

Swift is an independent artist who is turning to NFTs to support herself. It took months of research and marketing before she released her first collection,

Misfits, a collection of 33 prints that used the same photo negative and were painted over by an anonymous artist friend.

Swift says the process was difficult but, “the hardest most time-consuming part had absolutely nothing to do with creating the art, and it had everything to do with promoting the heck out of myself.”

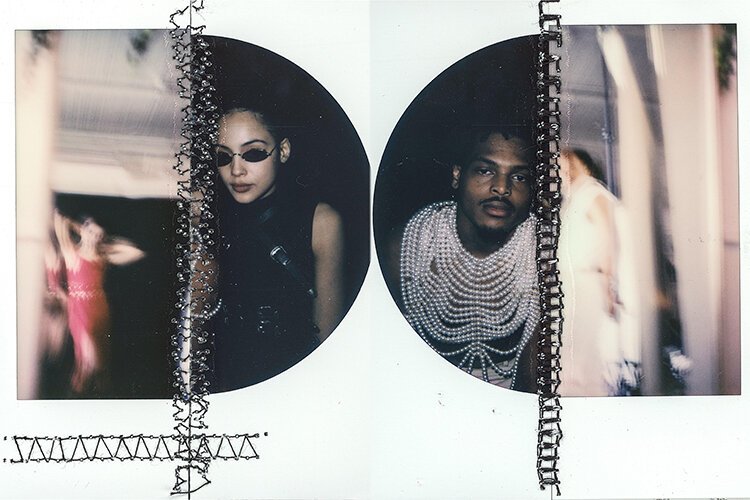

![]() Emily Swift's collection SYZYGY is a multimedia collection of 66 1/1 Polaroids. Photo: Supplied/Emily Swift.

What is an NFT?

Emily Swift's collection SYZYGY is a multimedia collection of 66 1/1 Polaroids. Photo: Supplied/Emily Swift.

What is an NFT?

An NFT is a digital item that has a unique identifier, acting as a digital certificate of authenticity. The identifier cannot be duplicated or forged, as it is stored in a blockchain.

A

blockchain is powered by a collective of computers that keep track of sales of both digital and physical objects, often referred to as a digital ledger. It works by using blocks of data that continue to build upon each other, and transactions are made with digital money, like Bitcoin, called cryptocurrency.

The rise of blockchain technology has created a tangible value for digital goods and artwork, with the marketplace currently valued at

$41 billion. An NFT is not a physical item, which means copies can still be made, but the original carries a digital signature that verifies ownership of the original digital copy. One way to view it is that the NFT is the original artwork and copies online are much like prints.

It paid off for Swift. All 33 of her prints sold out within 45 minutes. The prints were listed at .33 Ethereum a piece,

over $1,400, at the time of the sale.

“I looked at my friend when it sold out, we literally cried,” Swift says. “We could pay our rent. We could feed ourselves a good meal and we didn't have to worry for a couple of months. That was a feeling, that as artists, we have absolutely never been able to comfortably feel by means of strictly just selling artwork.”

NFTs worked for Swift. However, they have also led to disruption and disaster for others.

The decentralized nature of the NFT market has allowed criminals to exploit it. A common scam, a

Rug Pull, introduces a new cryptocurrency or NFT to mint. After gaining enough investors, the creators drop the currency or NFT and disappear with the investors’ money.

Artistic control is another concern. The minting of an NFT does not always require the original creator, and some plagiarized pieces have been released.

Opensea, the leading seller of NFTs,

says this year that a minting tool led to “over 80% of the items created with this tool [to be] plagiarized works, fake collections, and spam.” Most of these illegal sales were initiated by bots. The freedom of the new market means regulation and prosecution are difficult.

![]() Steve and Dorota Coy are the husband and wife conceptual and visual artist duo behind Hygenic Dress League Corporation.

Detroit dives in

Steve and Dorota Coy are the husband and wife conceptual and visual artist duo behind Hygenic Dress League Corporation.

Detroit dives in

Another example of an investment with NFTs is happening in Detroit. A conceptual art project,

Hygienic Dress League (HDL), is planning a public offering with shares distributed as NFTs.

HDL was started in 2007 by Dorota and Steve Coy in what they describe as “a new and original form of art” and their first NFT, “First Contact,” sold for $100,000 in December.

Shareholders in the new initiative will receive their shares as unique NFTs featuring “employees” of the company. The shareholders would be entitled to 4% of the royalties of any additional sales of the NFT.

This new public offering is a follow-up to their

initial offering in 2014 which distributed shares as gold-papered stock certificates. HDL is seeking less traditional investors and is hoping to engage the general public more in this new offering.

Is it just another trend?

NFTs have been around for nearly a decade, dating back to 2012 with the creation of

Colored Coins and then to Kevin McCoy and Anil Dash creating the first true NFT in 2014. In 2017,

CryptoKitties introduced the world to the economic potential of NFTs. Certain “kitties” were selling for as high as $100,000.

NFTs hit a record peak in February 2021 when Christie’s, one of the world’s leading art auction houses, sold an NFT titled “

Everydays: The First 5000 Days” for over $69 million.

The market continues to grow. Sales have

increased by $20 million per 30-day period from just a year ago. During the COVID-19 pandemic interest in digital media has increased with

half a million users added each day. It’s keeping Swift hopeful.

“Artists don't have retirement funds,” says Swift. “We don’t have 401ks. We kind of are in a position where we have to take care of ourselves.”

However, the risks of cryptocurrency might eventually outpace any investment. Roughly 50% of every $1 in Bitcoin results in some form of climate or health damage in the U.S., according to a 2020 study from

Science Direct. As NFT transactions increase, the study says there is a potential to reach a point where the environmental cost of Bitcoin overtakes its economic value.

What to watch out for

One of the challenges of NFTs is how they’re paid for. NFT sales require both buyers and sellers to use cryptocurrency. Opensea uses Ethereum for example. Sellers and buyers have to navigate all the different currencies, wallets, and exchanges. Coupled with a volatile market it can be a hurdle for newcomers. The value of Bitcoin

dropped by nearly $10,000 over the month of January alone.

There have also been similar claims about revolutions in digital commerce with social media and sites like

Patreon. While these options have given artists more reach neither have proved to be as profitable as NFTs. Yet, they are a reminder that new marketplaces often overpromise.

Most sites require a minting fee to put the NFT on a marketplace and Swift says she had to pay around $3,000 to sell her collection after all the fees. She used a Smart Contract which gave her more control and guaranteed her a

royalty standard – each time the NFT is resold a percentage of the new sale goes back to the original artist.

Even with her success, Swift says people should not be naïve about the risks. The $3,000 was a lot for her to invest but she had a partner and could afford the risk at the time.

“It's hella scary to put a lot of trust and hope into such a volatile market and into such a new method for selling art. I really encourage people to do their research and to go into it knowing what could happen, both good and bad, so that you have realistic expectations. Don't drain your bank account on Ethereum to release something because you just don't know what will happen.”

Since the marketplace is still new, unique challenges appear to be popping up every day. With tax season coming up, Swift still isn’t sure how to claim her gains from the sale.

“It's tricky as far as like making sure you file taxes correctly,” Swift says. “I did speak with a crypto financial advisor about everything, and it varies state to state. Essentially, it’s like being paid in shares. It’s a little different for all of us.”

As NFTs create new possibilities and problems, Swift says it’s more about what artists do with the market than the market itself.

“We kind of are in a position where we have to go find it ourselves. NFTs have given us a beautiful place for that to happen. But they can also leave us stranded. It’s important to keep putting yourself out there. Push your story, push the work and the rest will follow.”